/ Research, Publication, DeFi

Contagion and loss redistribution in crypto asset markets

Publication by Katrin Schuler, Matthias Nadler and Fabian Schär in Elsevier's Economics Letters

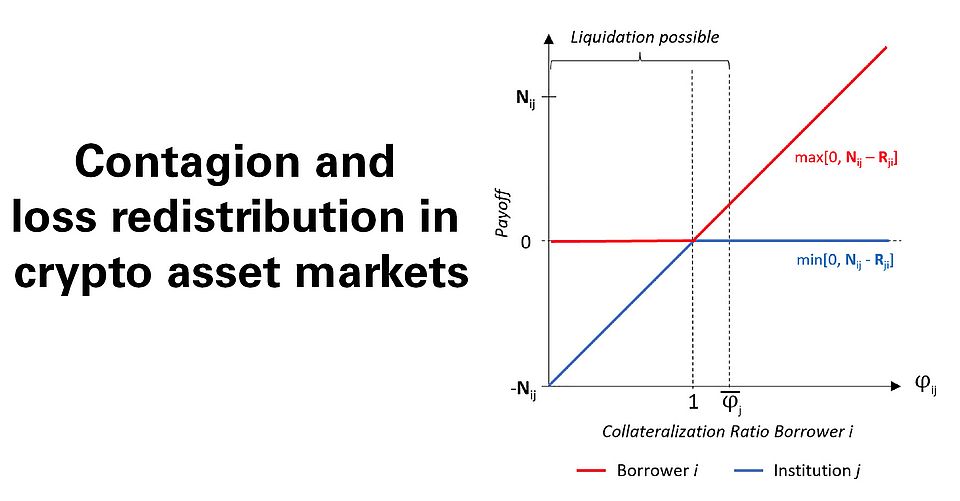

This paper addresses the growing concern of shock propagation in crypto asset markets. The integration of conventional financial institutions (CeFi) and decentralized financial protocols (DeFi) has introduced a set of complexities that are not adequately accounted for in current models. We build on the well-established framework by Eisenberg and Noe (2001) and propose a generalized extension that can be applied to mixed DeFi/CeFi networks. Our model serves as a tool for comprehending potential contagion channels and loss redistribution resulting from the non-recourse nature of DeFi loans.

Highlights:

- Investigation of decentralized and centralized finance (DeFi/CeFi) intersection.

- Extension of model by Eisenberg and Noe (2001) to DeFi/CeFi mixed network.

- Integration of DeFi characteristics around non-recourse loans and liquidations.

- Framework to measure loss redistribution between institutions, savers, and borrowers.

- Crypto market interconnectivity is a major contributor to shock propagation risks.